|

|

|

|

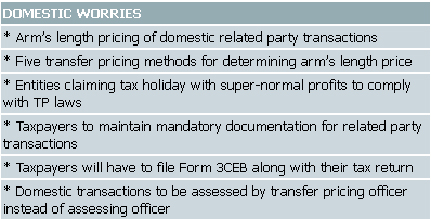

Pandora's box opens with domestic transfer pricing SEZ NewsTax liability, costs of mid-sized firms to go up SEZ, realty firms to be hit Companies with cross-border operations were adversely affected in the financial year due to high transfer pricing, a new international field of taxation. In the budget 2012-13 the finance minister incorporated domestic transactions in the transfer pricing for the first time to improve the scenario for the next financial year. "The tax base (for transfer pricing) will simply double. Earlier, it was only cross-border transactions of multinationals. Now, it will cover all related party transactions. For multinationals, compliance doubles as they have to report even transactions between their domestic arms," said Ajit Tolani, associate partner, Economic Laws Practice. The companies with operational units in SEZ and having policies to take the maximum advantage of applicable tax holiday by investing their bulk profit in these will be affected. Real estate firms, which route transactions through hundreds of subsidiaries and associate companies, will also need to comply with transfer pricing documentation and reporting norms. An amendment in the finance bill redefined the international transactions by including "specified domestic transactions" of Rs. 5 crore and more in it. Transfer pricing officers will do a scrutiny for transfer of goods and services between related parties, extraordinary profits and profits earned by SEZs. "Transfer pricing will not be limited to just the large groups any more. Many mid-sized groups, partnership firms, Hindu Undivided Families (HUFs) and even individuals in smaller cities will now have to adhere to the TP rules," said Samir Gandhi, partner-transfer pricing, Deloitte Haskins and Sells. "This will lead to an increase in the administrative and compliance burden for the taxpayer in respect of such transactions and a focused examination by the tax authorities."

"The above amendment has opened a Pandora's box for taxpayers, with specified domestic related party transactions," said a post-Budget note by Economic Laws Practice (ELP). The penalty for non-compliance has also been made severe. Earlier, it was a flat fee of Rs 1 lakh for not reporting a transaction irrespective of its size. At present, the penalty is two per cent of the transaction. Thus, even if one forgets to disclose a transaction of Rs 5 crore, which is the minimum threshold for reporting, the penalty is Rs 10 lakh.

In addition with this, the finance minister has also incorporated transactions such as valuation of intangibles, capital financing and provision of services under the definition of "international transactions". Consultants say that the capital financing could appear as a key area in domestic transfer pricing. Presently a number of domestic companies make inter-corporate advances and give guarantees to group firms. At market rates, these transactions attract charges of three-four per cent. These charges will be supplementary to the taxable income. "TP officers will put to use all lessons learnt from foreign firms over the past 10 years. They know exactly where to attack. Questions will be raised on routing of transactions through multiple entities, and adjustment entries," said Tolani of ELP. "The whole system will be cleaner." |

The latest amendments have extended the concept of arm's length pricing to these transactions. The move was in line with a Supreme Court recommendation in the case of CIT versus Glaxo SmithKline Asia, the Finance Bill said.

The latest amendments have extended the concept of arm's length pricing to these transactions. The move was in line with a Supreme Court recommendation in the case of CIT versus Glaxo SmithKline Asia, the Finance Bill said. Some lawyers point out that the Advance Pricing Agreement (APA) introduced to reduce disputes will not cover the domestic related party transactions, making the plight of local firms even more severe. "While the APA regime has been introduced with respect to international transactions, the same benefit has not been extended in cases of domestic transactions," Nishith Desai said in the note.

Some lawyers point out that the Advance Pricing Agreement (APA) introduced to reduce disputes will not cover the domestic related party transactions, making the plight of local firms even more severe. "While the APA regime has been introduced with respect to international transactions, the same benefit has not been extended in cases of domestic transactions," Nishith Desai said in the note.